The year 2024 left many challenging as well as optimistic approaches, especially for the equipment industries. On the one hand, the demand for equipment is skyrocketing due to the rapid initiatives of infrastructure and residential building construction, while on the other hand, the prices of heavy equipment are going beyond the reach of the buyers, making them resist investing in heavy-duty machines.

In this uncertain situation, the OEMs are trying their best to bring more user-friendly deals to help the buyers. It is quite important to keep a strict eye on the market trends for all the buyers and stakeholders.

How did the market look like in December 2024?

All the individuals connected to the equipment industry for any reason, know that the industry has experienced some noticeable change in the past few years. There are several reasons for this fluctuation including the rising fuel prices, and unstable economic and political situations.

Despite all this, knowing the fluctuating market trends will help you make wise judgments whether you’re in charge of heavy-duty or medium-duty equipment.

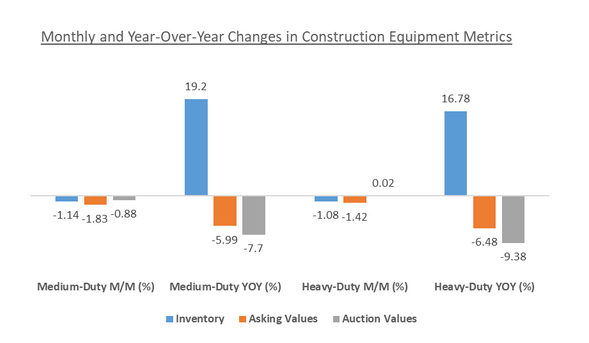

The medium-duty equipment market is consistent with minor fluctuations

Medium-duty construction equipment is always in demand and hence its inventory level is majorly affected.

However, in December 2024, it saw a decline in month-over-month (M/M) sales by 1.14%, whereas the Year-over-Year (Y/Y) sales increased by 19.2% which is one of the most amazing data to note.

If we talk about the skid steer inventory, the fluctuation was recorded by 3.33% M/M in a declined pattern and a rising pattern in Y/Y by 29.17%. The expert states that this indicates the demand for this category of equipment is still intact and not going anyway down in the few next years.

In the meantime, asking values have been declining. They fell 1.83% month over month and 5.99% year over year in November, with used backhoe loader for sale suffering the biggest dip at 3.48% month over month.

Similar downward trends were seen in auction values, which fell 7.7% year over year and 0.88% month over month.

Whereas, loader backhoes once again saw the biggest decline, down 3.35% M/M. At 12.38%, wheel skid steers saw the biggest year-over-year drop in auction values, indicating a difficult market for sellers but a favourable one for buyers.

The heavy-duty equipment segment has seen major fluctuations

In November, the market for heavy-duty equipment gave some uncertain and conflicted patterns. Inventory levels are still 16.78% higher year over year, despite a minor M/M reduction of 1.08%.

Surprisingly we have seen a major shift in the wheel loader category with almost 32.03% Y/Y rise in inventories whereas a decline in M/M by 2.05%. It is a clear indication that the supply of this category of equipment is higher in the market which will put further pressure on sellers to again change the prices.

Crawler excavators showed durability in this segment, as seen by their 2.7% M/M increase in auction values.

Wheel loaders, on the other hand, saw the biggest year-over-year decline in auction value (10.5%), suggesting that this category may provide some deals, however, things are still uncertain.

1400 Broadfield Blvd, Houston, TX 77084,

USA.

1400 Broadfield Blvd, Houston, TX 77084,

USA.

WhatsApp +1-713-304-6013

WhatsApp +1-713-304-6013